Overall, from a markets' standpoint, the May CPI figures are encouraging and support our view that the Fed will cut the policy rate two times by year-end. (UBS)

On the CPI front

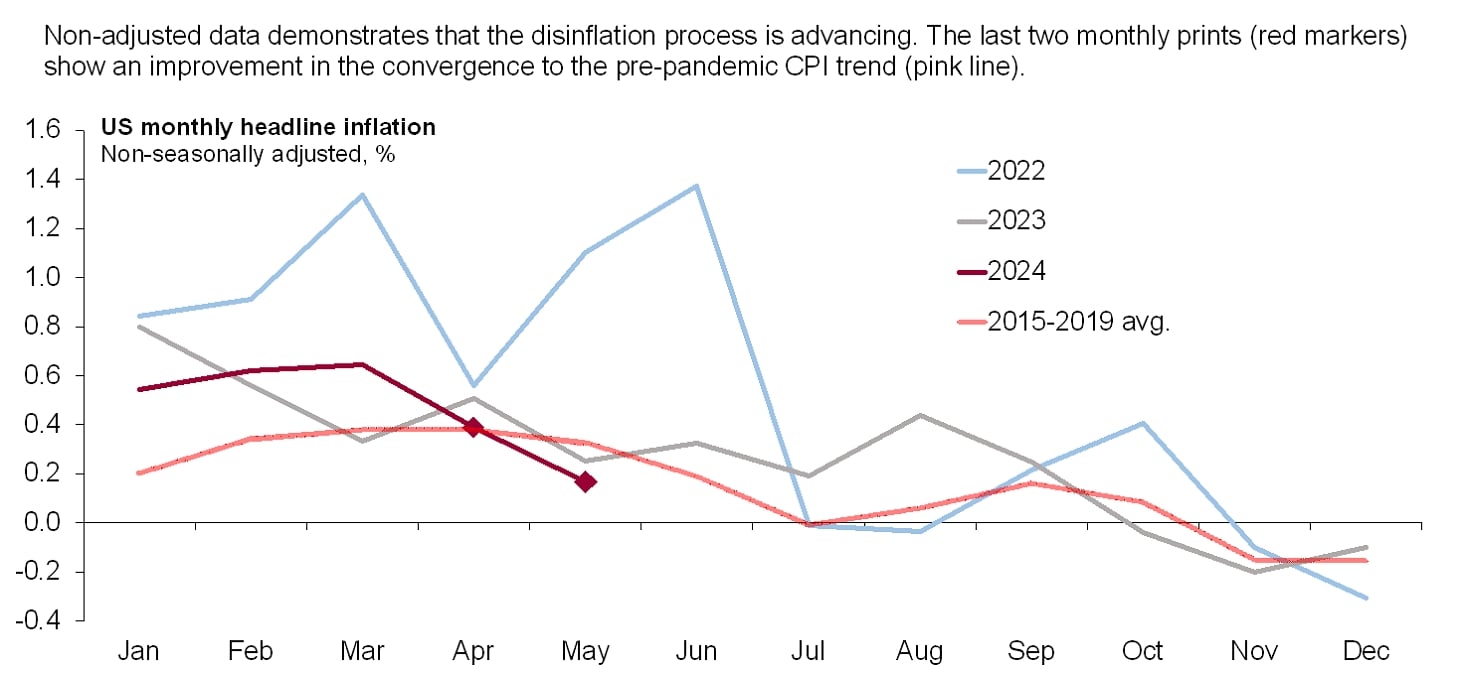

Headline inflation was flat (0.0% m/m) in May, below market expectations of a 0.1% m/m increase. On its part, core inflation was 0.2% m/m, also surprising to the downside relative to consensus of 0.3% m/m. Noteworthy moves included deflation prints in airfares, gasoline, and auto insurance. Yet, owners’ equivalents rent was 0.4% m/m for the fourth consecutive month, still displaying a somewhat troubling stickiness.

In annual terms, headline inflation was 3.3% in May, down from 3.4%. Similarly, core inflation fell to 3.4%, from 3.6%. Our initial estimates for core PCE—the Fed’s preferred inflation measure—suggest a print of 2.6% y/y, continuing the downward trend seen over the past 18 months. Furthermore, preliminary data shows that a softening of inflation is likely to continue in June.

Overall, from a markets' standpoint, this was a positive inflation report. CIO’s head US economist, Brian Rose, highlighted that: “The way the data surprised to the downside was very favorable to the Fed”.

Fed decision and the dot plot

Moreover, the FOMC left the monetary policy rate unchanged yesterday, in line with expectations. The most important part, though, were the revisions to its forecasts (also known as the dot plot). The FOMC median expectations now call for only one policy rate cut in 2024. Notably, though, a significant amount of policymakers (8 out of 19) projected two cuts.

In the press conference, Fed Chair Jerome Powell underlined that the latest inflation report certainly showed progress in inflation and helps to build confidence among the committee. Moreover, Powell noted that economic activity is cooling as expected and that the Fed will continue with a data-dependent approach.

Market reaction

In the words of our Head of Tactical Asset Allocation, Jason Draho: “the market reaction was two steps forward, one step backward.” Following the CPI release there was a widespread rally in US equities and fixed income, but the move pared back somewhat after Fed decision and Chair Powell’s press conference. As the markets closed, the S&P 500 was up nearly 1%, while US treasury yields rallied about 8–10bps.

However, Jason added that “the direction of travel is still toward cuts, which should be beneficial for risk assets”. In line with this, the curve is now pricing 44bps of cuts by year-end, roughly 10bps more than a few days ago.

Bottom line

We stand by our base-case that the Fed will cumulative cut 50bps in 2024, with the first move in the September meeting. In this context, we think there is a constructive outlook for US equities. Our year-end target for the S&P 500 is 5,500, and we favor the sectors of information technology and industrials.

From the fixed income standpoint, we reiterate our bias toward quality. We expect high quality bonds to deliver solid total returns in 2024, as the decline in yields becomes more pronounced in the second half of the year. Specifically, we see good value in US TIPS, investment grade corporate bonds, Agency Mortgage-Backed Securities, Commercial Mortgage-Backed Securities and municipal bonds.

For more, listen to:CIO First Take: May CPI data & FOMC meeting

Jason Draho, Head of Asset Allocation Americas, and Brian Rose, Senior Economist Americas, share thoughts and reflections on May inflation data, along with the outcome of the FOMC meeting. Jason also speaks to the market response, and shares CIO’s positioning recommendations. Host: Daniel Cassidy

Main contributor: Alberto Rojas, Investment Communications Writer — CIO Americas